|

|

|

|

|

|

In this month's X Report, Brighteye Ventures share findings on 'Learning for the over 50s' and the opportunity this market presents in Europe, and we explore the technology skills gap and market activity within the technology skills sector. Each month we share a snapshot of key trends, showcase the stars of today and tomorrow, offer our insight on mergers, acquisitions and fundraising, as well as providing some further food for thought.

|

|

|

|

|

Learning for the over 50s: Untapped opportunity in Europe?

David Guérin, Principal at Brighteye Ventures

At Brighteye, we believe that “disrupting the way older people learn and socialise” is an overlooked and truly exciting market opportunity in Europe. We recently published a market map (15+ companies) and an investment thesis on this space, which you can read and access here. Today, we would like to share with you a more digestible version of that research. Let’s dive in.

I) Five market tailwinds for senior people in Europe

From a macro perspective, this market opportunity is pushed by five macro drivers:

- Ageing European population:

Today ~30% of the population (~90m people) is >55 years-old and by 2050, this age class will represent ~42% of the total population (140m people).

- “New generation” of older adults is digitally connected:

The elderly population is clearly increasing its digital skills and online presence. Their online behaviours changed considerably in terms of online communications between 2009 and 2020.

- Spending behaviours and increased income:

The median equivalised net income for European older adults grew by 18% between 2012 (€14.1k/year) and 2020 (€16.7k/year).

- New online habits and COVID effect:

Lockdowns were a forcing function and according to Google in the UK, “a majority of online seniors spend at least six hours a day online and own an average of five devices.”

- Increasing age of retirement:

The normal age of retirement in Europe is being pushed up by most countries to 65 years old, which is forcing workers to stay in the workforce longer.

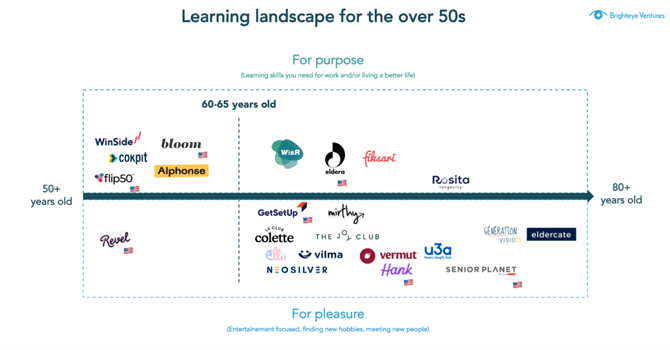

II) Who are the players in this nascent market

We have found 15+ companies in Europe that are trying to serve and disrupt this overlooked population. These European companies collectively represent less than €15m raised from VCs and as indicated on the market map below, they can be categorised into two major groups: (1) learning for purpose and (2) learning for leisure.

Interestingly, we found that these solutions are primarily built on five attributes:

- Social (i.e. making meaningful connections, sense of belonging and connecting with other people)

- Trust (i.e. safety, quality and human interaction)

- Ease of use (i.e. simplified UX/UI to get straight to the core value of the solution)

- Flexibility (i.e. the notion of freedom seems to be key for retired people)

- Embracing being an “older adult” (i.e. people in later life don’t want to be made to feel old by brands. Quite the opposite in fact, they want to feel seen and heard by the brand)

III) Where to invest: six [potential] themes

Based on this high level analysis and on interactions with a number of founders who are trying to disrupt this space, we found several themes that could unlock the market opportunity for senior people.

- Theme 1: Unlocking and accessing the wisdom, insights and hard-to-access knowledge of older adults for younger generations

- Theme 2: Allowing retired people to increase their monthly income by making extra money

- Theme 3: Navigating the pre-retirement phase

- Theme 4: Building edutainment platforms with a strong focus on human connection

- Theme 5: Finding new hobbies and/or learning new skills with their peers: “By Seniors, For Seniors”

- Theme 6: Allowing seniors to raise their profiles and be seen as “cool”

The whole Brighteye team would like to congratulate and encourage all the passionate entrepreneurs who are building companies in this exciting and nascent space. You can access the full piece here.

Also, if you are or know someone who is building a learning/edutainment platform for the 50+, feel free to reach out (dg@brighteyevc.com). Thank you to all the founders who have contributed to this piece!

|

|

|

|

|

Addressing the Pressing Technology Skills Gap

Digital transformation has been catalysing the need for technology skilling across industries. It is estimated that by 2030, there will be a global human talent shortage of more than 85 million people, equivalent to c.$8.5 trillion in unrealised annual revenues1. Consequently, over 150m new tech roles are required by 2025, with software development, data analysis, followed by machine learning, being most demanded2.

The launch of Microsoft’s .Net framework in 2011 was one of the first globally recognised training providers. Since then, there has been a proliferation of both accredited and unaccredited providers seeking to service the technology skills gap globally. The majority of new providers supply solutions that address immediate skill gaps at entry level, rather than provide a holistic career pathway. Learners seeking technology skills include K12 students, fresh graduates, upskillers, and career switchers.

e-Learning courses are the most prevalent solution, where technology skills are taught by instructors or asynchronously where content is self-paced. In terms of Indian EdTech giants operating in this space, UpGrad, Simplilearn and Great Learning provide accredited degrees and unaccredited courses partnering with global universities. There are also intensive bootcamps delivered on-campus or online; for example, IronHack is online and has 9 on-campus locations. Further, a multitude of career services seek to support the learner journey, from mentorships with experienced peers to specialist interview preparation and job marketplaces.

Programs which are longer and require more involved teaching command a higher price from learners. One of the highest noted was c.$20,000 upfront for an eight-month unaccredited career mentorship course. Thus, income-sharing agreements are increasingly implemented to mitigate the high upfront cost for learners, commonly in US and India. Pathrise requires no upfront payment and charges 5-18% of the learner’s salary across the initial years after a job is secured.

On the employer side, Recruit-Train-Deploy (RTD) provides solutions for companies to source and train their talent pipeline, typically charging a staffing or placement fee to the employer. Code First Girls works with 100+ corporate clients across various industries to train and source diverse tech talent via courses at no cost to learners.

Another notable trend is the growth of solutions for K12 students, particularly tutoring and games to supplement the core curriculum of schools that have been slow or unable to adapt to the need for technical skills.

To address the skills gap effectively, a variety of solutions is required across all learner life stages, tech skilling verticals, accreditation levels, delivery methods and price points. In our view, this sub-sector will continue to show promising growth and consolidation in the years to come.

For the full IBIS EdTech report on Technology Skills, please contact nt@ibiscap.com

1Korn Ferry 2021

2Microsoft Data Science 2020

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| M&A Activity > |

|

|

|

| Significant Fundraising Activity > |

|

|

|

|

|

Industry Analysis – Technology Skills

Key Points

Transaction activity within the Technology Skills sub-sector has been growing over the past 5 years, with 2021 experiencing a record year for deal making by volume and value. In 2021, there were c.215 companies in the space that engaged in transactions, whether fundraising or M&A, with a cumulative disclosed transaction value of $6.4bn. Across 2018 to 2020, there was an average of 173 transactions per year, with disclosed transactions averaging at $1.3bn in 2018-19, which increased by 1.8x to $2.4b in 2020 and grew by 2.7x to $6.4bn in 2021.

.jpg?upscale=true&width=600&upscale=true&name=Chart%201%20(1).jpg) .jpg?upscale=true&width=600&upscale=true&name=Chart%202%20(1).jpg)

The majority of deals in the space were led by strategic peers in other EdTech verticals looking to join the technology skilling space. For example, to expand its existing K12 maths subjects and exam prep, BYJU’s has begun a rigorous rollup strategy with the $200m acquisition of Tynker (K12 coding games), the $600m acquisition of Great Learning (online degree-level and certificate courses), and the $300m acquisition of WhiteHat Jr (K12 online coding tutoring).

Traditional staffing and human resources companies have also shown interest in this space, evidenced by Adecco’s acquisition of General Assembly, in an effort to grow its education offering via synergies with corporate training services for its enterprise clients. Synergies between strategic acquirers also command a multiples premium. The Great Learning-BYJU'S transaction saw an EV/Revenue multiple of 13.7x and similarly, the Thinkful-Chegg transaction traded at an EV/ Revenue of 7.1x.

In January to October 2022, there has been c.72 fundraises in the technology skilling sub-sector globally. The majority of funds raised within the technology skilling companies were in the United States and India (31% and 28%, respectively), which comes as no surprise, with the prevalence of established and up-and-coming service providers to meet the demands of a large addressable market. The UK, Japan and Australia are also other active markets within the fundraising space.

.jpg?upscale=true&width=600&upscale=true&name=Chart%203%20(1).jpg)

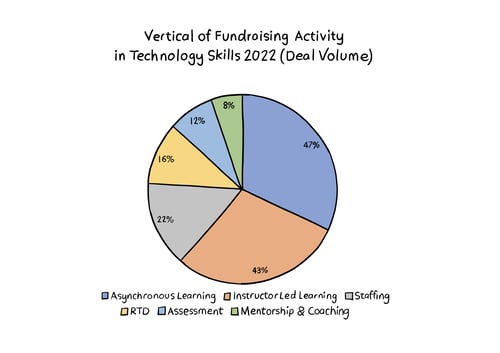

In terms of 2022 fundraising based on Tech skilling verticals, 61% of funds raised by volume has been driven by e-Learning solutions – with asynchronous learning and instructor-led teaching accounting for 32% and 29% of fundraising volume respectively. 2022 has also witnessed the growth of recruit-train-deploy (RTD) and staffing solutions, which together accounted for 25% of fundraising by volume.

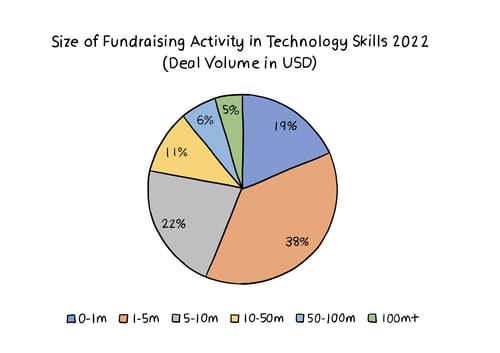

Nearly 40% of the fundraising volume in 2022 came from a round size of between $1m-5m, with a large number of early-stage companies seeking capital to fuel further growth. On the other end of the funding size spectrum, companies who have successfully raised over $100m in 2022 include Multiverse, Masterschool, Upgrad and Emeritus.

Over the next 12-24 months, we expect to see increased transaction activity with the advent of new solutions coming to market to address the pressing technology skills gap. Existing providers are expected to target larger funding rounds in conjunction with increased M&A activity as larger companies seek to exit or consolidate via acquiring smaller assets in the space.

For the full IBIS EdTech report on Technology Skills, please contact nt@ibiscap.com

Sources: CapIQ, Tracxn, IBIS Capital Proprietary Database as of October 31st 2022

|

|

|

|

|

|

|

|

|

|